By Jim Cline and Kate Kremer

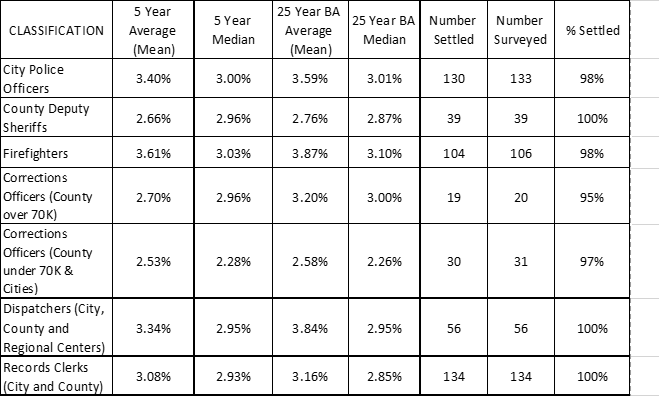

This is the third part of our 2021 wage series. In this article, we take a look at recent contract settlements and examine how those trends vary from recent previous years. Our view of 2019 and 2020 settlements and what we have so far from 2021 indicates that the Washington State public sector wages dropped in 2021 but not as substantially as employers might suggest. We see some wage increases with little substantial “real wage” growth (as measured once controlled for inflation). Whether a growing economy eventually will accelerate these is something we’ll discuss later in this series.

This is the third part of our 2021 wage series. In this article, we take a look at recent contract settlements and examine how those trends vary from recent previous years. Our view of 2019 and 2020 settlements and what we have so far from 2021 indicates that the Washington State public sector wages dropped in 2021 but not as substantially as employers might suggest. We see some wage increases with little substantial “real wage” growth (as measured once controlled for inflation). Whether a growing economy eventually will accelerate these is something we’ll discuss later in this series.

In

In

A year unlike any other, health care has been at the center of our attention. What does that mean for insurance costs going forward? Always an important part of the negotiated total compensation, we’re also paying attention to the trends in health care costs.

A year unlike any other, health care has been at the center of our attention. What does that mean for insurance costs going forward? Always an important part of the negotiated total compensation, we’re also paying attention to the trends in health care costs.

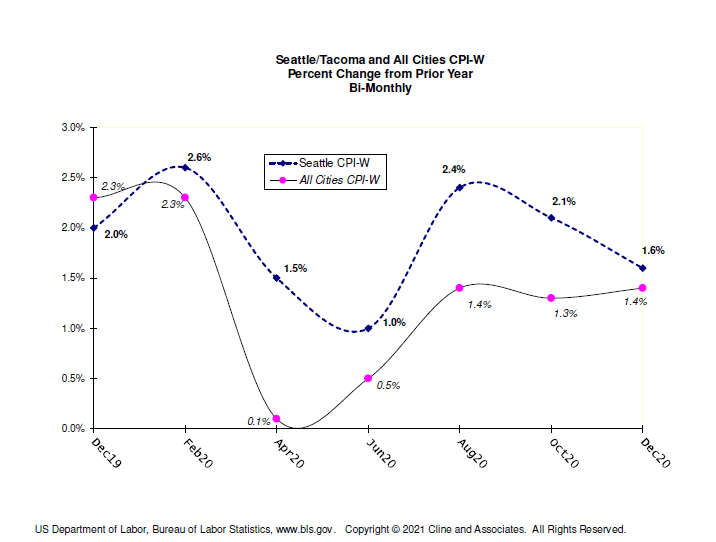

Despite the pandemic and the associated recession, inflation has not completely disappeared, especially in the Seattle metropolitan area. This chart shows the month to month changes in the Seattle and All Cities “W” index from October 2019 to October 2020:

Despite the pandemic and the associated recession, inflation has not completely disappeared, especially in the Seattle metropolitan area. This chart shows the month to month changes in the Seattle and All Cities “W” index from October 2019 to October 2020:

By: Jim Cline and Kate Kremer

By: Jim Cline and Kate Kremer