By Jim Cline

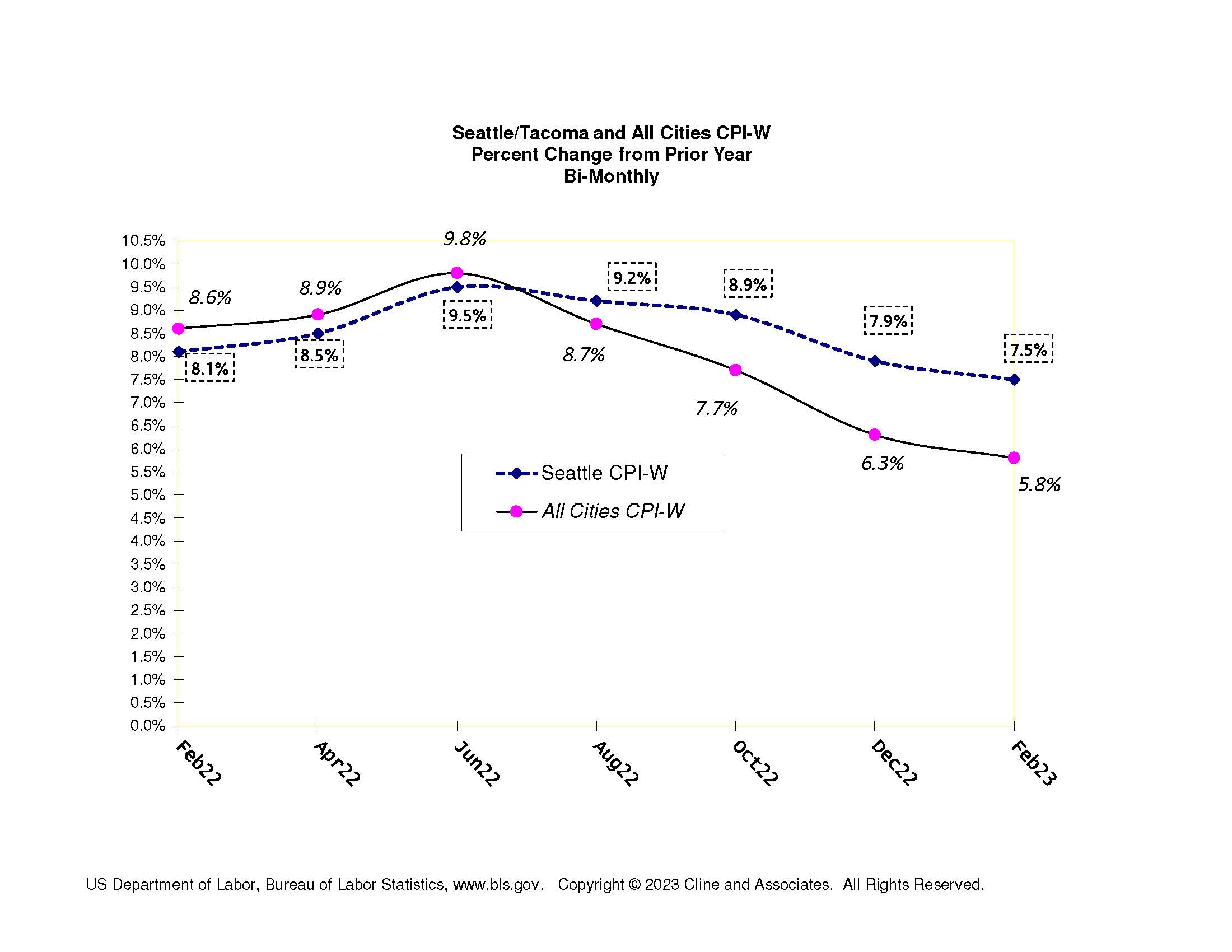

In our last newsletter we discussed the most recent CPI reports. It discussed the slowing but still high inflation numbers. This chart shows the 12-month trend line in the Seattle and All Cities CPI:

In our last newsletter we discussed the most recent CPI reports. It discussed the slowing but still high inflation numbers. This chart shows the 12-month trend line in the Seattle and All Cities CPI:

In our January webcast we had a detailed presentation about current and future direction of inflation and how we anticipated that would impact current and future negotiations. We discussed the recent direction of contract settlements. We also discussed economists’ predictions that CPI would slow significantly heading into mid-2023.

The Fed is clearly attempting to curtail inflation by throttling the money supply. The expected impact of restricting the money supply is to slow economic growth and, in theory, the rate of inflation. It’s been widely discussed that they risk triggering a recession to do so. But the Fed clearly has determined that continued inflation is a greater risk to the economy than a predicted shallow recession.

For most 2024 contract negotiations, the mid-year June CPI number is the most important gauge for what would be considered the “cost of living” adjustment. To the extent labor contracts use CPI as a measure, the June number is the most frequently incorporated index. As we’ve explained:

While we watch each periodic CPI Report to assess the inflation trend line, the June number is particularly important because it has more influence on the following year’s contract negotiations than other CPI Reports. While CPI is just one (albeit significant) factor driving contract settlements, the June number has more impact than any other month’s numbers because, of those Washington public safety labor contracts which tie their “out year” wage increases to a specific CPI formula, the June report is by far the most frequently chosen month used in formulas.

In the latest (January) Wall Street Journal survey of economists , the median prediction for the National June 2023 was a drop to 3.6%. Given the more recent CPI reports, there’s some doubt that in the remaining 4 months before that report is generated that the 3.6% estimate will match reality. Based on a variety of inflation indicators (direct and indirect) that we’re observing, we are anticipating that the June number may be over 5%.

The other complications for Washington labor negotiations is that the Seattle CPI is outrunning the All Cities number by about 2 points. The latest (February) BLS survey reported the Seattle-W index at 7.5%. The less frequently relied upon Seattle-U index came in at 8.0%.

As we have explained, the “Seattle” denomination is often misunderstood. The BLS survey region for the “Seattle index is the broader Seattle Metro area reach including all the central Puget Sound counties. As a result, the Seattle index, despite employer resistance, is widely used not only throughout I-5 counties but often throughout the State.

We have frequently discussed the history over the past 20 years of the Seattle CPI outrunning the national numbers. As we explained in 2016:

This certainly does not mean that the Seattle index will outperform in all cycles or indefinitely in the future. There may well be, and in fact likely will be, future economic cycles where the Seattle economy and CPI index under-perform relative to the rest of the nation. But we have been advocating use of the Seattle index almost consistently over the past 20 years and that has been proven. Our last discussion, Seattle CPI Still Appears to Retain Edge over All-Cities CPI Index, demonstrated that the Seattle index had outpaced the All Cities index by 2.8% in a 10 year cycle.

Will the Seattle Index outperform the All-Cities index over the next 10 years? At this point, that would be difficult to predict. But we certainly are anticipating the Seattle index to outperform for at least the next few years. There are a number of factors impacting regional variation in inflation rates, but the strength of the local economy is undoubtedly the strongest factor. With all current indicators suggesting a continuation of the Seattle mini-boom, we have no reason to believe that the Seattle inflation will fall below the national rate in the near future.

We are seeing a more recent trend, particularly outside the Seattle Metro area, for a greater reliance on one of the various West Coast or “West” indices. These indices had been running a bit ahead of the All-Cities numbers but more recently they’ve fallen closer in line.

In the next article in this series, we’ll drill down further on how these inflation developments may impact current and upcoming negotiations.