By Jim Cline and Kate Kremer

The latest inflation numbers were reported by the Bureau of Labor Statistics last week. The numbers have been edging down and the December CPI numbers coincide with predictions that the CPI will continue to fall and return to normal over the next year.

The latest inflation numbers were reported by the Bureau of Labor Statistics last week. The numbers have been edging down and the December CPI numbers coincide with predictions that the CPI will continue to fall and return to normal over the next year.

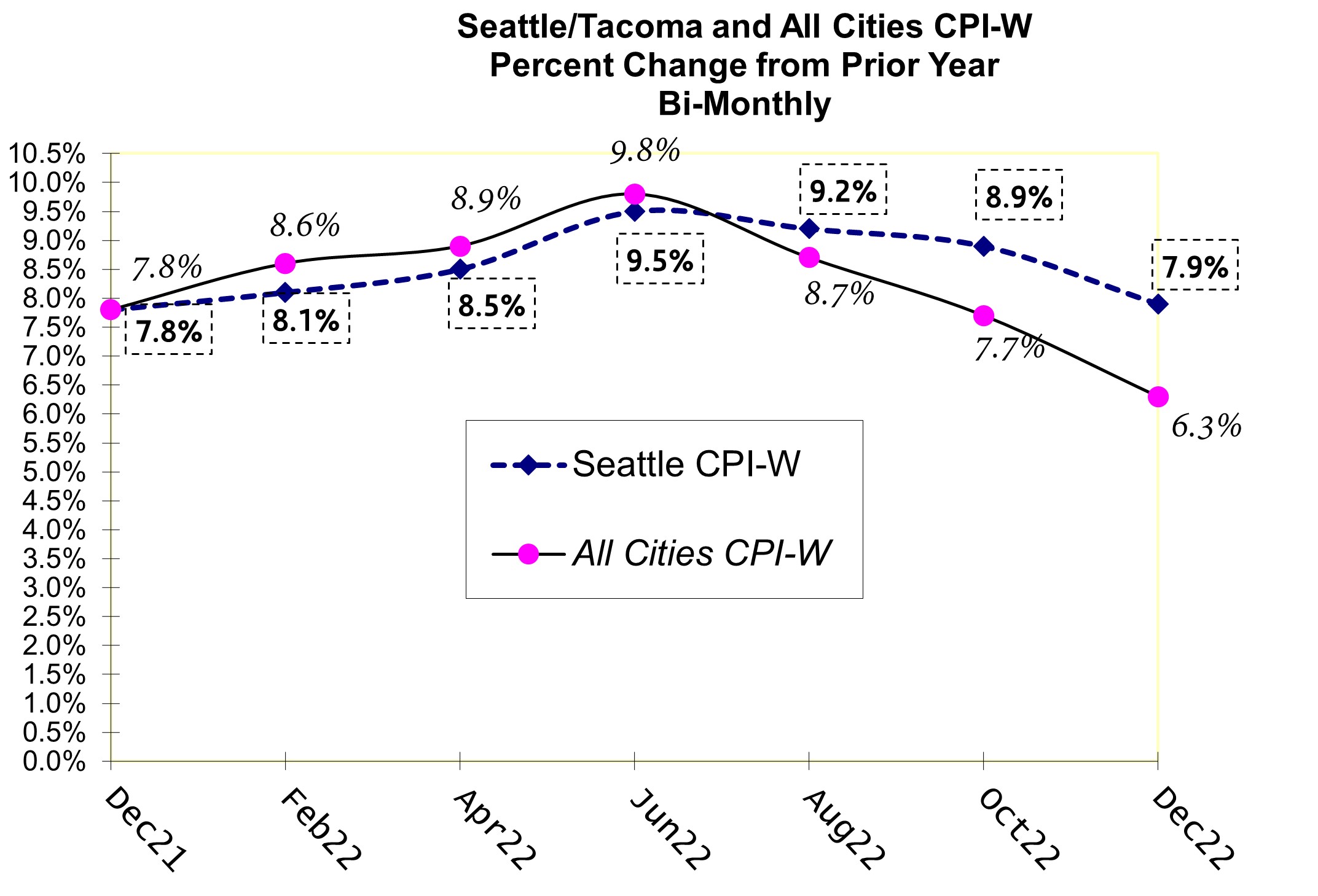

The All-City W CPI was reported at 6.3%. The Seattle number came in a surprisingly higher 7.9%.

The fact that the Seattle number outpaced the national number wasn’t surprising. What was surprising was by how much.

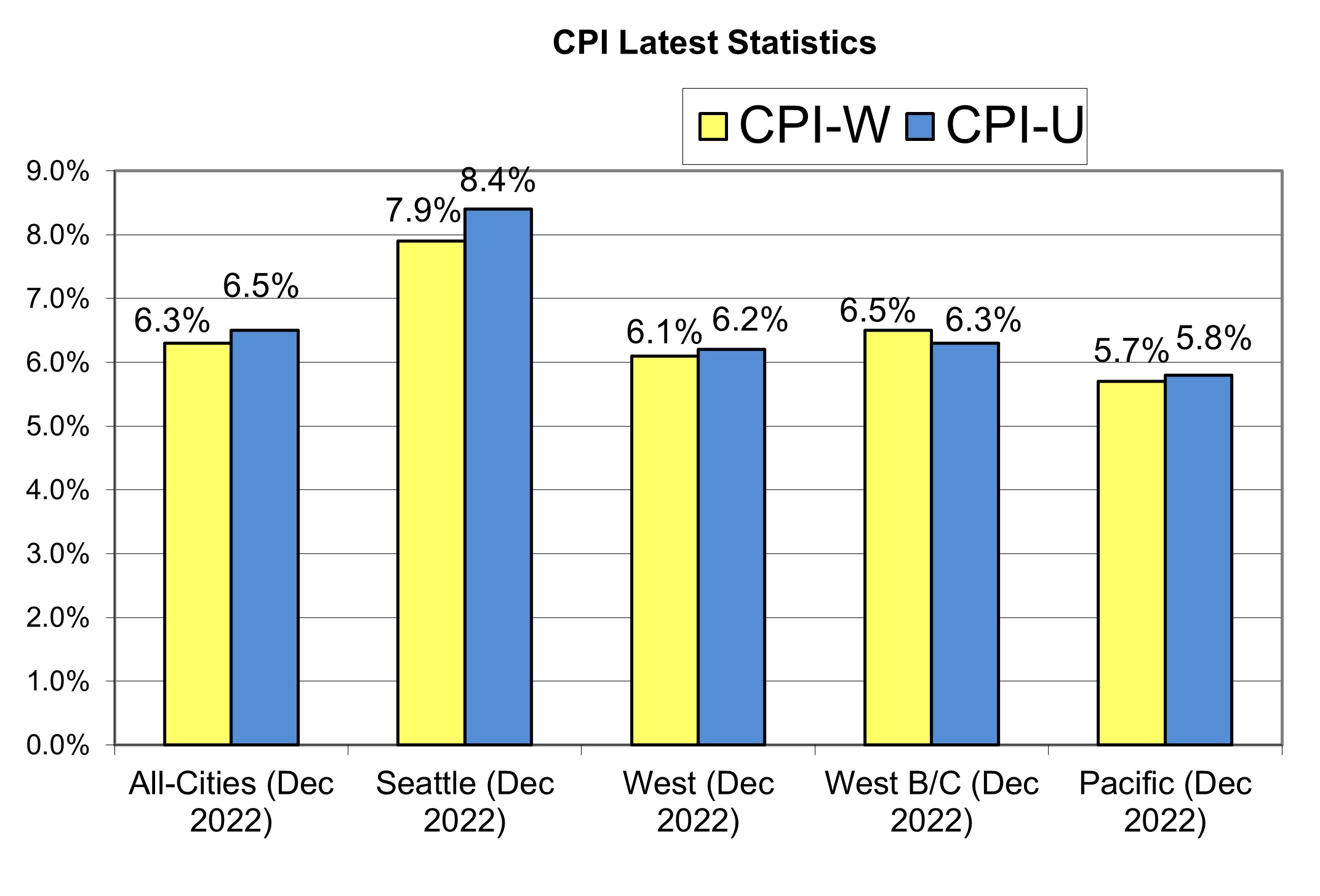

Beyond the often-used W numbers shown above, the chart below also reports the CPI numbers for other inflation indices often used in Washington public safety contracts (and compares those numbers to the peak June 2022 numbers):

Will the Seattle numbers continue to ride higher? We find it noteworthy that the other indices that measure large West Coast cities seem to be falling closer in line with national numbers even though they’ve also been riding high in recent years. Local economic news might suggest that Seattle numbers will eventually subside. The current round of tech layoffs seems likely to reduce the high pressure that’s persisted in Seattle area rents. Those rents have been a major factor in the All Cities v. Seattle differential.

As always, we would note that the “Seattle” index is not just for the City of Seattle. It’s a regional index taking in most of the Puget Sound area under BLS sampling methods. Therefore, it’s a very common index to use throughout Western Washington and even Statewide.

The larger question that looms over these new numbers is — which directly is general inflation heading? We covered that a bit in yesterday’s Cline and Associate’s Webcast. We’ll be producing some articles as a follow up to the latest Webcast to discuss what the prevailing economic wisdom is as to the direction of inflation (and how that will impact your contract).