By Jim Cline and Kate Kremer

The latest CPI data shows a continued easing in inflation. The period of higher inflation of the past few years seems to be ending at least for now. And the large gap that had existed between the City and All Cities CPI also seems to be closing.

The latest CPI data shows a continued easing in inflation. The period of higher inflation of the past few years seems to be ending at least for now. And the large gap that had existed between the City and All Cities CPI also seems to be closing.

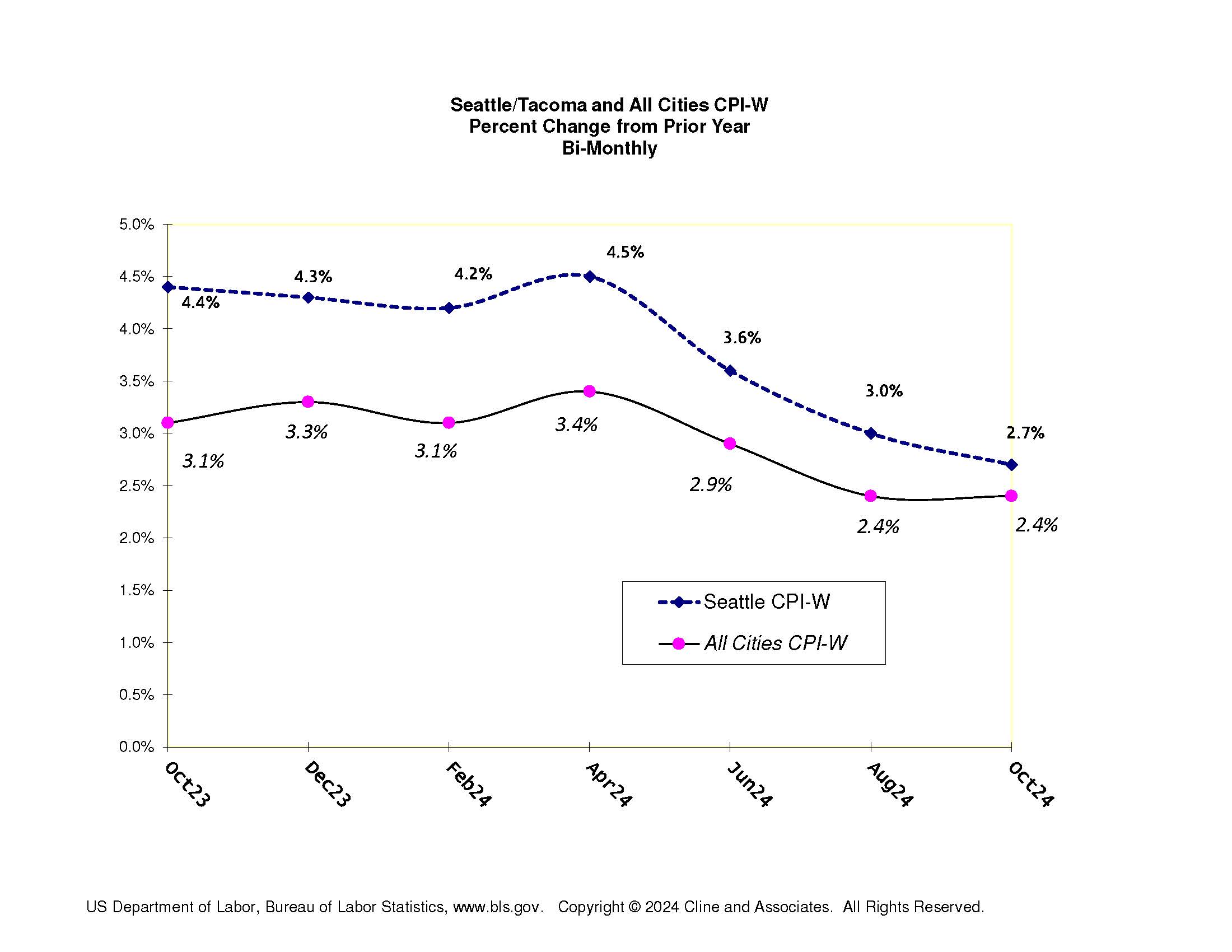

This chart shows the most recent CPI released earlier this month by the Bureau of Labor Statistics, along with the 12-month bi-monthly numbers:

For most of the past year, the Seattle CPI has outpaced the national numbers by more than one percent. A year ago, the Seattle and All Cities W index were 4.4% and 3.1%, respectively. As shown, those numbers are now 2.7% and 2.4%.

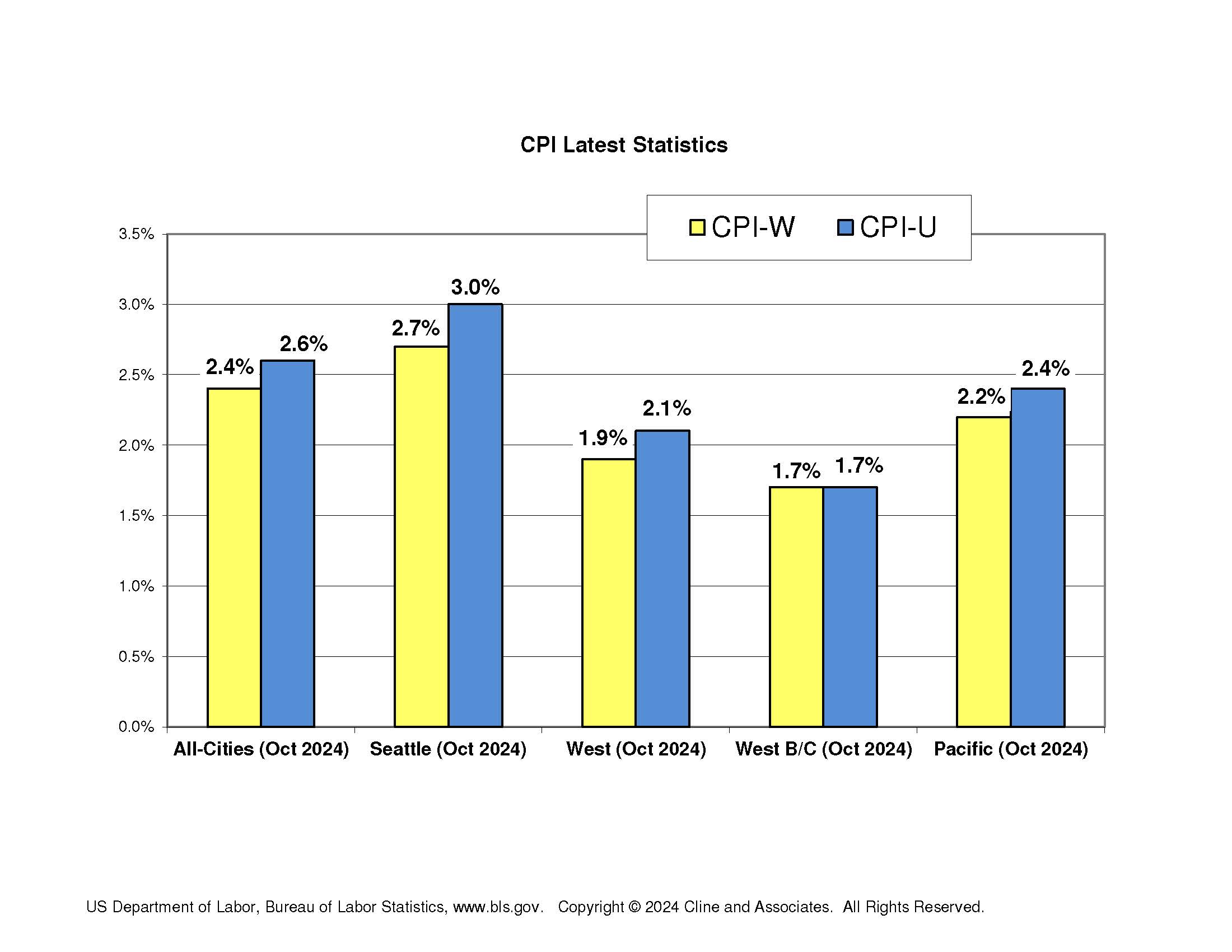

Here’s a summary of both the “U” and “W” numbers on a range of CPI formulas most commonly used in Washington public safety contracts:

Since the heightened CPI over the past few years has led to an increase in overall settlement trends, we are anticipating these new, lower numbers will likely lead to a reduction on those trends. But there are many variables impacting those trends. One major factor is that a number of jurisdictions which settled contract at far less than CPI over the past few years are likely to negotiate for some type of “catch up” increases. So far, the preliminary data we are seeing for 2025 settlements show many settlements at 4% or more. We will follow up with another report soon on those developments.